A 401(k) is a great benefit normally associated with large companies where the employee makes contributions and the employer offers a match. The contribution limits are high (and total max contribution of 56k for 2019) and can allow for significant tax deferral on the income you earn each year. What a lot of people may not know is that you don’t have to be a large company to have a 401(k) plan. In fact, you can be the only employee in your own business and have a retirement plan.

A 401(k) is a great benefit normally associated with large companies where the employee makes contributions and the employer offers a match. The contribution limits are high (and total max contribution of 56k for 2019) and can allow for significant tax deferral on the income you earn each year. What a lot of people may not know is that you don’t have to be a large company to have a 401(k) plan. In fact, you can be the only employee in your own business and have a retirement plan.

If it is just you in your business, your company can start a retirement plan known as a solo 401(k). The solo 401(k) allows you to adopt a retirement plan and make personal as well as company contributions to the plan for yourself and any of the owners of the company.

- You must have a business generating ordinary income to make to have a 401(k) plan.

- You can personally contribute up to $19,000 to the plan.

- Your company can contribute up to 25% of the income it pays you.

- For 2019 the total max 401(k) contribution is $56,000.

The 401(k) plan can be self-directed, which means you can invest the funds in almost any opportunity you find (subject to a few exceptions centered on collectibles). The 401(k) also has a loan provision allowing you to borrow funds from the plan and use them for anything you want.

If you have employees that are over age 21 and work more than 1,000 hours, you can’t have a solo 401(k). When this is your scenario you can still have a retirement plan, you’ll just have to allow the employees to participate and make matching contributions to them if you plan to do the same for yourself. You will need a Group 401(k) plan if you can’t have a solo 401(k).

What If I have Multiple Businesses With Only Employees in Some?

If you have multiple businesses and some have employees and some don’t, you will need to be aware of the controlled group rules which govern whether or not you can have a 401(k) in one business without offering it to the employees in the other business or group. The rules for this are infinitely more complex than those laid out above for solo or group plans. If you know you are in this situation, you should continue on below. The short answer though is that if you own all of the businesses and have no other significant partners, you will have to offer the plan to employees in all companies. But what if you own some companies entirely and have some partners in others? Well, read on, but beware the rules are very complex. We try our best to break down the common scenarios.

Controlled Group Rules

The crux is this: If you or your business are a member of a controlled group, you can’t make contributions to a retirement plan without offering the same to the employees in the controlled group. The classic scenario, a lawyer has a paralegal and legal secretary working for him (probably doing most of the work while lawyer golfs or skis). Lawyer wants to add a solo 401(k) to save for future ski and golf, and calls us. We say yes, you can have a group 401(k) plan but lawyer is not ready just yet to contribute the employees’ retirement. Lawyer devises a plan: I will create a separate law firm as the parent company of my current firm, with zero employees, and will rule also the world!

The IRS and Department of Labor saw Lawyer’s plan, so they made rules about leaving employees out of retirement plans in such a fashion. A controlled group happens when two or more corporations, trades or businesses (including partnerships and proprietorships) have one of the following relationships: Parent-subsidiary, Brother-sister or a Combination of parent-subsidiary and brother-sister.

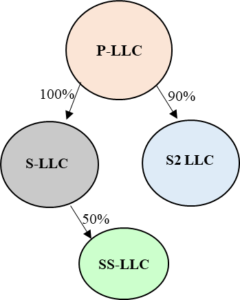

- The first rule is the parent-subsidiary. If you have a parent company with a controlling interest, regardless of the entity type (or lack thereof), in any subsidiary company you have a controlled group. To have a controlling interest the parent must own or control eighty percent (80%) of the total shares, membership, or profit or capital interest. The graphic shows a parent subsidiary control group. If any of the entities have employees, a 401k plan in any other entity has to be available to any of the employees.

- The second rule, a brother-sister controlled group test is met when you have (1) Five or fewer individual (including estates and trusts) (2) own a controlling interest in each organization, and (3) have effective control. The new term here is effective control which means 50% or more of the companies control is held identically in all companies.

| Membership | S3-LLC | S4-LLC |

| Individual A | 80% | 20% |

| Individual B | 10% | 50% |

| Individual C | 5% | 15% |

| Individual D | 5% | 15% |

| Total | 100% | 100% |

The controlling interest is met here because the same 5 or fewer individuals own 80% or more of the membership. However, remember this test has three parts! The third part, the effective control is not met! Thus no brother-sister control group. The identical interest in each LLC is only 40% when all are added together.

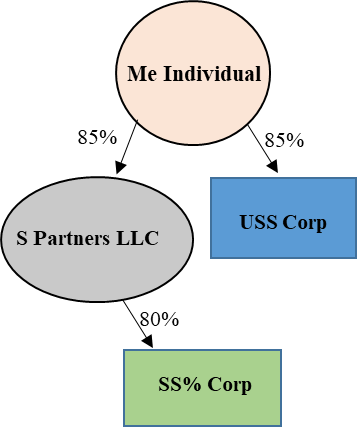

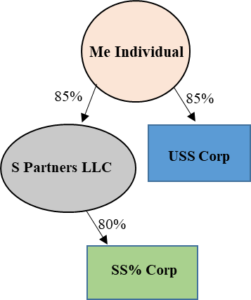

- The third type of controlled group is a combined controlled group. A combined control group happens when you have a parent-subsidiary or a brother-sister controlled group and at least one parent is part of the parent-sub and is also a part of the brother sister controlled group. The below and to the left diagram is an example of this.

Each of the companies are part of a controlled group because they have a parent sub or a brother sister controlled group (Me individual, S partners, and USS Corp) and S Partners is the parent that is part of the brother sister controlled group. If you are in this spot, or you think you may be close, call us and we will walk you through it.

The final two pieces to this are infinitely more complex. The IRS has constructive ownership rules that apply to control groups as well. Basically, any business ownership of members of your family is attributed to you for purposes of the controlled group tests. If you fall into this category, you will need to call us for sure to discuss the specifics.

Finally, the original example of the lawyer was not just because I play one on TV (or want to). The IRS has rules about affiliated services groups for certain service industries because we…ahem… they always have layers of ownership that could disguise this situation and potentially evade the controlled group rules. If you are a doctor, lawyer, accountant or really any professional service provider and you principally provide a service to produce income you could be an affiliated group and have to provide retirement benefits to employees in another entity.

In the lawyer example, let’s say the lawyers start a partnership that owns a law firm. The law firm “contracts” with another entity formed to partner with the law firm to provide paralegal services to the law firm, but the lawyers don’t have any actual employees, nor does the law firm. However, this is an affiliated group and any contributions to 401Ks have to be made available to the employees in the separate company, even ignoring the other controlled group rules.

The bottom line is this is complex because we have become complex trying to determine ways as entrepreneurs to build up our retirement. If you land anywhere close to any of the above examples, and would like to see what can be done to save some taxes and build your retirement we want to help. Keep in mind that the advice may well be that it is time to make the plan available to your employees, and that isn’t all bad either. It shows your growth and demonstrates your commitment to continued growth with the right people.