by Kevin Kennedy | Feb 10, 2020 | Business planning, Retirement Planning, Securities law

Many of you are familiar with rolling over a former employer 401(k) to an IRA. This is very common. But does it ever make sense to do the opposite, i.e., roll over/ transfer an IRA to a 401(k)? This is sometimes called a ‘reverse rollover’, and the answer is YES. Here...

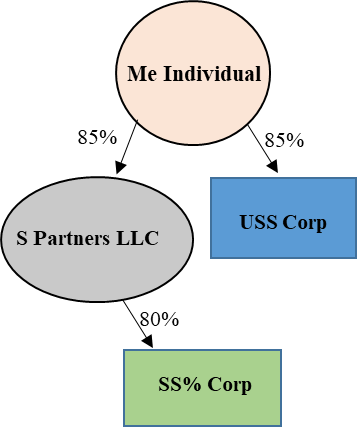

by Deven Munns | Dec 11, 2019 | Estate Planning, Law, Real Estate, Retirement Planning, Small Business, Tax Planning

Deven L. Munns, Esq. Opportunity Zones (OZ) investments were created under the recent passage of the Tax Cuts and Jobs Act (TCJA) and designed to help states jumpstart communities that historically have struggled economically. In theory, they have a two-prong benefit;...

by Mat Sorensen | Feb 4, 2019 | Business planning, Retirement Planning

A 401(k) is a great benefit normally associated with large companies where the employee makes contributions and the employer offers a match. The contribution limits are high (and total max contribution of 56k for 2019) and can allow for significant tax deferral on the...

by Deven Munns | Jun 5, 2018 | Asset Protection, Business planning, Estate Planning, Retirement Planning

Many people ask us on a regular basis ‘who’ is going to carry out their wishes when they’re gone. All of us should have a Will or Trust, but the ‘people’ that are going to implement it can be a big question mark sometimes. It’s...

by Lee Chen | Mar 13, 2018 | Estate Planning, Law, Retirement Planning, Uncategorized

Life insurance is an integral part of financial and estate planning for many. In most cases, people purchase life insurance in order to protect their spouse, children, and/or others who are financially dependent on them from becoming indigent in the event they die....

by Lee Chen | Nov 6, 2017 | Retirement Planning, Tax Planning

For many Americans, saving for retirement is like exercising or eating healthy, we know we should do it but most of us don’t. In fact, a survey published by the Washington Post reported that over 70% of Americans are not saving enough for retirement and a study by...