I have a close relative who works in fund-raising for a fairly large university. While he loves receiving large charitable donations in the form of immediately available cash or other marketable assets (such as real estate and publicly-traded stock), he knows that such donations are often simply not possible or practical for the average person. This is why a huge buzzword in the world of fund-raising for non-profits is “Planned Giving.”

I have a close relative who works in fund-raising for a fairly large university. While he loves receiving large charitable donations in the form of immediately available cash or other marketable assets (such as real estate and publicly-traded stock), he knows that such donations are often simply not possible or practical for the average person. This is why a huge buzzword in the world of fund-raising for non-profits is “Planned Giving.”

What Is “Planned Giving”?

Planned Giving is the present day legal commitment by a donor to give some assets or property to a charitable organization or institution at a future date. The future date is usually the death of the donor.

There are several types of planned gifts. Some people make outright gifts of assets such as appreciated securities or real estate. Some planned gifts are payable upon the donor’s death such as a life insurance policy where the beneficiary is a charitable organization. Still other planned gifts provide a financial benefit, as well as a tax deduction, for the donor. Examples of this are: 1) Charitable Remainder Trusts, which provide an income stream for the donor, and at the death of the donor, the charity receives what is left in the trust; and 2) Charitable Lead Trusts, which essentially do the opposite and produce a stream of income for a charity, and the donor’s heirs receive what remains in the trust when the donor passes away.

What Is a Charitable Remainder Trust (“CRT”)?

A CRT is a tax-exempt irrevocable trust designed to reduce the taxable income of individuals by first dispersing income to the beneficiaries of the trust for a specified period of time and then donating the remainder of the trust to a designated charity. If you have a highly appreciated asset (e.g. real estate), the CRT will avoid capital gains taxes that would otherwise be due if you or your company sold the asset.

Who Should Be Thinking About a CRT?

People who:

- Have a highly appreciated marketable asset (usually real estate or stock);

- Want to save on taxes (i.e. they don’t want to take the capital gains tax hit);

- Want an income stream over the rest of their life or over a certain number of years;

- Want to make a donation to charity; and

- Want to totally or partially disinherit their children. This isn’t the case if you structure it correctly!

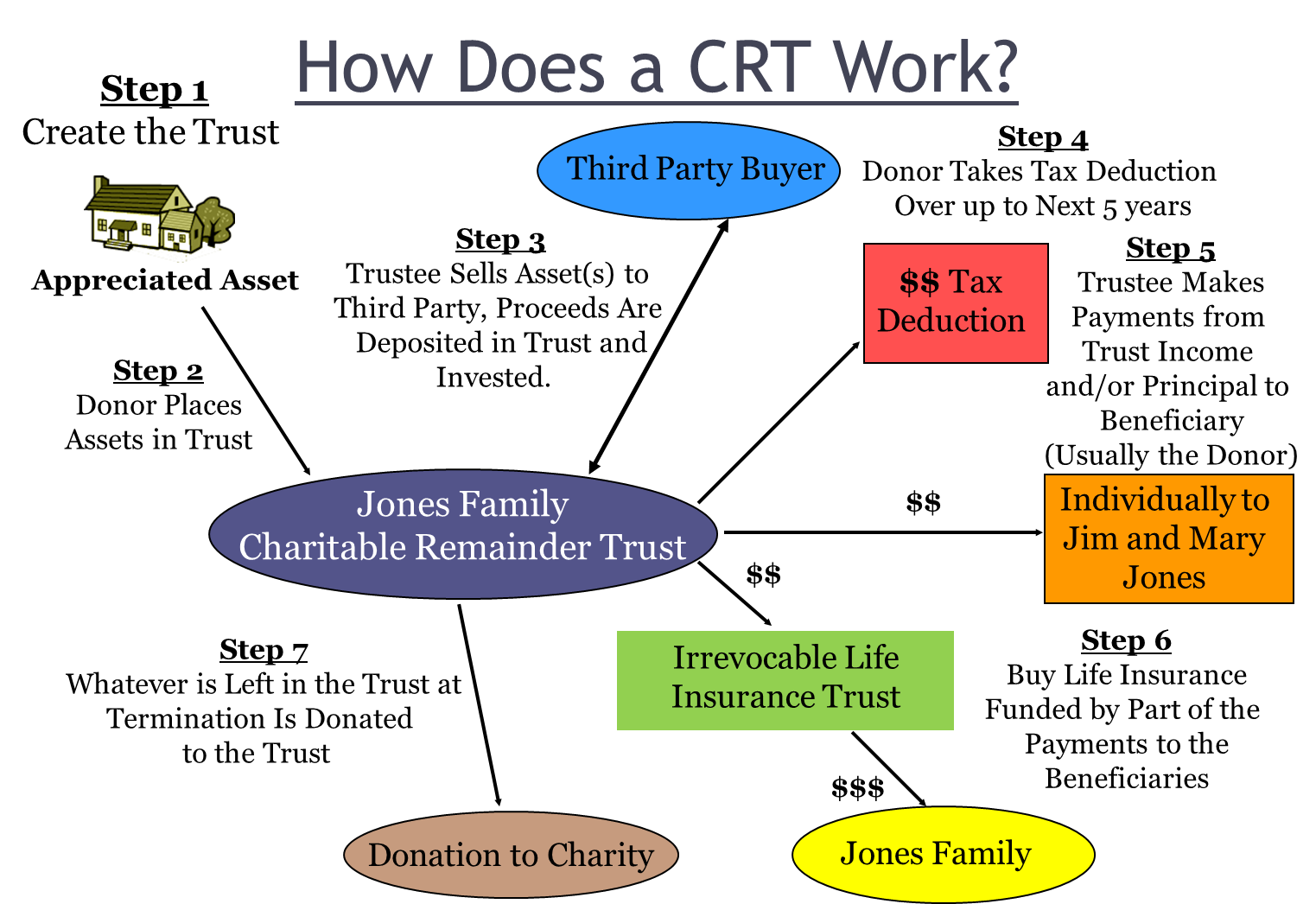

How Does a CRT Work?

The diagram below goes through the steps involved in a CRT. However, in a nutshell:

1) A tax-exempt trust is created with the help of a professional.

2) The donor places the asset in the CRT. Are taxes due here? No – and the donor gets a charitable deduction for making the donation that he/she can carry forward for up to five years!

3) The property is sold to a third party and the proceeds are deposited into a CRT-owned account. Are taxes due here? Not if the property is owned free and clear! These proceeds are then invested, and no taxes are owned when those investments appreciate in value!

4) Payments in a set amount or set percentage are made from the CRT account to the donor on a regular basis (quarterly, annually, etc.). Payments are either made for the life of the grantor or for a term of years. Are taxes due on this income? Yes, but the charitable deduction gained when the donation is made can be used to offset at least some of this income!

5) The donor can use some of the income from the trust to buy a life insurance policy in order to make sure their heirs aren’t left out in the cold. Do beneficiaries owe tax when they receive life insurance proceeds? No!

6) In some cases, the life insurance proceeds may be in the multiple millions of dollars, and could cause an estate tax problem for the heirs. This issue can be taken care of by the proper use of an Irrevocable Life Insurance Trust (“ILIT”) – which is another subject for another day.

7) At the death of the donor, or at the end of the term of years, whatever remains in the CRT is donated to the charity. Does anyone owe taxes here? No!

Who Are the Winners and Losers in a Properly-Structured CRT?

1) The Donor – Winner! Because he or she gets to avoid the capital gains hit on selling a highly appreciated asset, gets a tax advantaged stream of income, and gets to make a charitable donation that gives them warm fuzzies – and may end up helping to get their name on a building at their favorite university!

2) The Charity – Winner! The charity gets an irrevocable promise from the donor to donate assets at some point in the future. With good investment of the funds in the CRT, the final donation to the CRT can end up being significant.

3) The Donor’s Heirs – Winners! Instead of inheriting a piece of appreciated real estate that they need to market and sell, they get tax-free life insurance proceeds, and will avoid possible estate tax issues if an ILIT is used.

4) The IRS – Loser (for once)! When properly structured, the only taxes paid in all of these transactions are those owed by the donor when they receive payments from the trust. However, the charitable deduction will offset at least some of this income.

Now, there are plenty of details to sort through, but please give me a call if you’d like to discuss the CRT further and find out if it is something that might make sense for you.